Digital spoils: are B2B and Services businesses falling behind?

Monday 09 April 2018Article

We serve some of the world’s leading disrupters. They want to know what new worlds there are to conquer, where the weak points in today’s models are in terms of customer needs or cost to serve and how they can transform these. They see pots of gold in digital.

For many, however, there is the prospect of spoilt ambition. There is constant pressure to squeeze their operations further in order to maintain and grow returns, but they must also find the resource and know-how to fully benefit from digital and not be a victim of it.

Having been early adopters of digital technology, B2B and Services have perhaps lagged their consumer, retail and media cousins in recent years. That is now changing.

How will digital impact my industry?

Digital is not new. Computers have been around for decades. So too have many of the latest manifestations of change associated with digital such as robots, drones and e-commerce. However, the compounding effect of innovation is accelerating the pace of change. Now is not the time to be behind the curve.

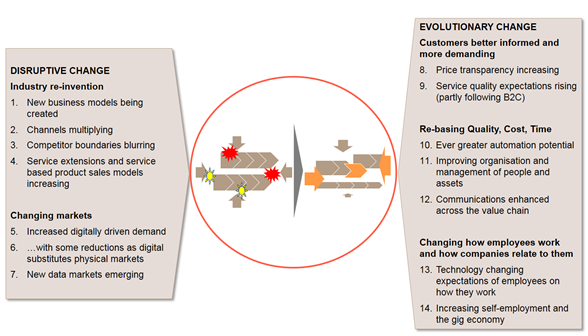

We would point to 14 types of impact on B2B and Services players:

Let’s look at some examples of these impacts today

- New business models being created

- The creation of a debt purchase industry by leaders such as Lowell harnessing ‘big data’ analytics to transform a very old industry

- The advent of on-line services shaking up established value chains such as Free2Convey offering all parties a ‘full chain view’ in conveyancing transactions

- Channels multiplying

- New entrants using omni-channel mastery to shake things up such as Screwfix in Tools and General Maintenance distribution

- Fleet managers now needing to fuse data from customers, drivers and the cars themselves

- Competitor boundaries blurring

- Amazon is growing in B2B in the form of Amazon Business whilst Amazon Web Services is shaking up the information technology industry

- Service extensions and service based product sales models increasing

- Zipcar offers consumers pay as you go whilst OEMs are betting on Transportation as a Service (TaaS), albeit many decades after Rolls Royce pioneered ‘power by the hour’

- Increased digitally driven demand

- Growth in drones add to the aerospace market driving demand in engineering services, testing, inspection, certification maintenance, repair and overhaul through life

- ...with some reductions as digital substitutes physical markets

- On the flip side, physical testing in many industries is being replaced by Computer Aided Design and Engineering with Ford aiming for zero R&D prototypes

- New data markets emerging

- Government’s making their data ‘open’ creates opportunities, with early examples showing the way covering a huge variety of applications from transportation to regulatory checks

- Price transparency increasing

- Customer visits to car dealers dropping from about 6 per sale in 1994 to 1 today as more and more the researching, comparing and even buying has moved on-line

- Fleet managers have been able to significantly reduce service costs using the Epyx platform to manage service and repair costs

- Service quality expectations rising

- At work people are demanding the same service levels that they get at home – with Amazon and others considerably raising the bar in terms of ease of browsing, ordering and delivery lead time and ‘window’ accuracy

- Distributors must focus ever more on On-Time In Full delivery performance rather than how much stock is in a particular branch

- Ever greater automation potential

- Automation is now moving into new areas of human activity including flying, driving and even software development

- So called ‘artificial intelligence’ is extending automation. Alexa and Siri have joined the conversation and look set to revolutionise how we interact with devices while Babylon the medical platform is supporting healthcare in some London Boroughs

- Improving organisation and management of people and assets

- The so called ‘Internet of Things’ allows tracking of people via their ‘things’ at a granular level and is moving beyond niche uses to become more mainstream with, for example, tracking movement and dwell times using Mobile Wi-Fi connections to highlight peel-off rates, visits and repeat visits or tracking passengers in the tube by TFL to illuminate routes through the network, and footfall

- GE sees such huge potential here that it is re-inventing itself by networking its asset base from trains to aero engines and establish itself as the leader in the ‘industrial internet’

- Communications enhanced across the value chain

- Visibility and communications end to end and at a granular level are now becoming common, not only enabling the tracking of stock and service equipment but also sensing abnormalities and scheduling corrective or mitigation actions fusing other technologies

- Technology changing expectations of employees on how they work

- Employees are increasingly expecting their work environment to mirror their personal environment, in terms of technology: the ways of communicating and collaborating with others at work should at least be as technology-enabled as the rest of one’s life

- Winning the best talent and ensuring they’re happy will mean utilising digital in a way that drives efficiency, flexibility and collaboration, using all forms of virtual work environments, multiple seamless means of communication on and offline, digital training and career management, and personalised tools for getting their jobs done

- Increasing self-employment and the gig economy

- 15% of the UK’s workforce are self-employed, many in the so-called ‘gig economy’ where they get paid per unit / service performed, but many also as high-skilled self-employed, who are seeking flexibility

- This new labour marketplace brings new dynamics of competition and the need to adapt to the way future generations view work and their relationships with ‘employers’

Where to begin?

Get informed: Do a quick scan on digital developments that will impact you today and in the future. This scanning is often happening across an organisation but not pulled together into a coherent picture

Clarify expectations: Be clear about what is expected from the strategic planning exercise and the explicit inclusion of digital within it with a premium on thinking outside the box to develop a vision but then also practical steps for the here and now to move things forward

Re-imagine the industry: Get the outsider’s view as well as those of customers and suppliers to avoid being blinkered and accepting of industry norms.

- Think about re-constructing the whole value chain, but also which profit pools within it you would target if you joined a start-up or competitor?

- Digital increasingly allows you to know things that seemed impossible before. What would you like to know?

Prioritise: Identify the most important potential changes to be addressed in strategy development whilst being open to different views from the organisation

Be explicit about data strategy: Review what data is most important and how it can be accessed, processed, secured and monetised. This is not an IT department task, but rather a strategy planning activity to make strong corporate assets out of an organisation’s data and also manages the risks associated with it

Plan for uncertainty: Develop a plan with different paths and a process to course-correct as things change. Identifying the pivotal changes that would cause you to re-think priorities is important. What would change your priorities? For example, many industries will be impacted by autonomous vehicles. For now they seem a distant prospect, but what if that were to change at least for certain areas?

Experiment, pilot and renew: Wholesale change is a complex and risky undertaking so it’s best to make sure the end state you are aiming for will work when you get there. Businesses will need to experiment and pilot new approaches. Your strategy should explicitly lay out how you will trial new ways of working, how you will set these up for success and how the organisation will maximise its learning from them to renew the whole operation based on a (more) proven view of the future

Organise for success: Organisational issues in terms of structure and culture will need to be overcome to really make change happen, work and stick. Which are the key elements of your organisation that you will need to change? Which will you need to keep?

Suggested Reading

Same day delivery: wrong for Uber, right for the brave

Uber has shut down its same day parcel delivery business, and in fact it never made it beyond three US test cities