Welcome to the Jungle: Amazon in Grocery

Friday 23 March 2018Article

Jeff Bezos has talked about winning in grocery for more than a decade, and last year’s $14 billion take-over of Whole Foods was a clear statement that he won’t be backing away from that ambition any time soon. As the news sunk in, there was much discussion about what Amazon would do with its new physical footprint, but it was, in the moment, just speculation.

Now, several months later, it is clear that Amazon has wasted no time: they lowered prices immediately at Whole Foods locations, introduced Whole Foods’ own label brand on Amazon, began offering special discounts in Whole Foods to Amazon Prime members, added Amazon Lockers and technology (Echo, Kindle) in Whole Foods stores, began integrating Prime into point of sales systems in stores, set up Amazon pop up stores within Whole Foods locations, and made buying at Whole Foods increasingly centralised and standardised. Most recently, they announced that in selected cities they will start delivering groceries from Whole Foods via their two-hour Prime Now delivery service, with the plan to expand the offering across the US this year. None of these is surprising, but the speed demonstrates their determination to blur the boundaries between the physical and digital worlds and roll out the algorithms and Prime membership that are such a big part of Amazon’s winning formula.

Prior to the acquisition, Amazon’s core grocery offer Amazon Fresh struggled to gain traction outside a few major metro areas, hampered by a lack of cold chain infrastructure, limited own label offerings, a brand that had little resonance in food, and no physical footprint for click-and-collect– indeed, they’ve now scaled back this service in at least nine states.

Gobbling up Whole Foods potentially solved some of those problems. But it’s only a starting point; it doesn’t immediately give Amazon the right to win in grocery.

It’s an accusation rarely levelled at the retail giant, but in grocery – an industry where scale is key – Amazon is still small. What’s more, the usual Amazon playbook doesn’t completely translate. “Limitless choice”, for example, isn’t a particularly compelling value proposition for most grocery shoppers.

Nonetheless, Amazon – through its pricing algorithms and its sheer presence – could pose a serious disruptive threat to grocery. What’s more, building a presence in Grocery has strategic value to the overall Amazon ecosystem as it deepens its interactions with consumers, improves the value and stickiness of Prime, and brings more traffic and data into the system to further power its famous “flywheel.” In short, it’s not going to go away anytime soon.

Suppliers therefore need to be agile as Amazon’s grocery offering develops further and alive to the challenges and opportunities this presents, now more than ever before:

- Whilst the question used to be “should I engage with Amazon”, this is no longer a debate – products will end up on Amazon regardless of approach, and disengagement is no longer a viable or attractive option. Instead the question is how to engage, without damaging brands or other channel relationships.

- Amazon doesn’t intentionally crash prices, but its pricing algorithm will expose ill-discipline in your customer management and pricing strategies. Transparency favours those with strong pricing control across customers and channels.

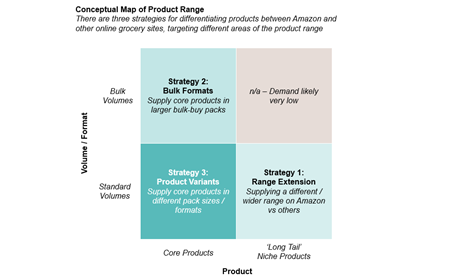

- Ranging strategies also come to the fore with increased transparency. We think about this along two dimensions: product and volume/format, the points of intersection of these lead to different potential strategies for managing the ranging dilemma. See figure below.

- Understanding how Amazon works and what they want from suppliers will be critical – they may appear to be just another channel, but they work differently than other customers, and we see a need for a different approach across many aspects of suppliers’ businesses, from investment strategy to relationship management to supply chain, all underpinned by strong analytics.

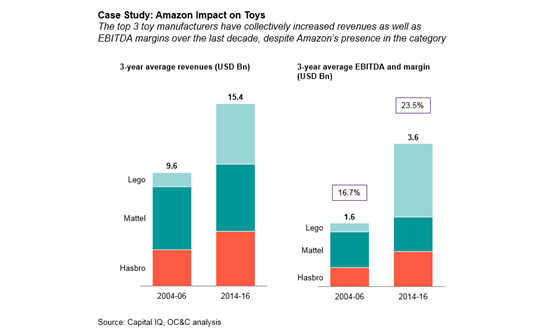

- When looking at other industries more developed on Amazon, such as books, toys, and electronics, we found that it was largely retailers that bore the brunt of the Amazon impact – strong manufacturers succeeded and profit pools remained. Beyond managing the pricing transparency, these successful suppliers have ongoing innovation that renews their offerings at new price points continuously, differentiated products and/or brands that mean something to consumers, and a strong focus on internal cost efficiencies. Amazon didn’t destroy the market – they just exposed the less fit amongst the competitors. See figure below.

If you want to learn more about how to respond to Amazon, don’t hesitate to get in touch.